Meeting the SDGs – How Will Bangladesh Play the Game?

Bangladesh has been lauded as one of the frontline nations to implement the Millennium Development Goals (MDGs) by achieving several targets ahead of time. Inspired by this success, the country set a vision to achieve the Sustainable Development Goals (SDGs) within 2030. Prior to the pandemic, Bangladesh was moving at a stable pace; however, the attainability of the SDGs remained a valid question. Adding to the uncertainty, COVID-19 has put a bigger question mark. Until 2019, the government’s “whole of society” approach that involves ministries, private sector, civil society organizations, non-government organizations (NGOs), development partners, and other stakeholders to carry out specific SDG related tasks has brought about mixed outcomes. While some goals like poverty reduction, gender equality, quality education, affordable and clean energy among others have gained momentum, some more ambitious goals like climate action, reduced inequalities, peace and justice are still at a rudimentary phase. To emerge as the next Asian Tiger, Bangladesh needs to metamorphose into a manufacturing-led economy from an export-led one and thus industrialization, innovation and infrastructure development (goal 9) will remain a top priority for the government in the coming decade.

Financing the SDGs: Over-Reliance on External Sources

Presently, 48% of the government’s ADP budget (USD 24.2 Bn) is being financed by external sources (project aid 35% and foreign borrowing 13%), while the rest is financed by revenue surplus (27%) and domestic borrowing (25%). [1] The comparatively lower interest rates and availability make foreign capital initially lucrative. One of the perils of relying on external sources is that it can dwindle given any change in the macro economy. For instance, the recent COVID-19 crisis has shrunk the loan and grants funds for Bangladesh to 46% compared to the same period in the previous fiscal year.[2]

One of the long-term repercussions of foreign capital is that the cost of the fund will keep rising and can be 15 to 20% more expensive compared to domestic capital in a ten-year time horizon due to currency devaluation. On top of that, as Bangladesh graduates to a middle-income country status in 2025, the flow of Official Development Assistance (ODA) will dry up and concessional loans will not have preferential rates anymore creating a fund vacuum. Simultaneously, the government has announced a stimulus package worth USD 12.11 Bn to subsidize different economic sectors in the wake of COVID-19. As a result, it is difficult for the government to increase spending on development programs on a great scale. Under these circumstances, mobilization of domestic sources to create a long-term development fund for financing SDGs can be explored.

Creation of a Long-term Development Fund: Mobilization of Domestic Sources

The 2030 agenda, with a capital requirement of USD 964.72 billion, additionally has two goals – mobilizing unprecedented volumes of resources and leaving no one behind. The government and other UN agencies are envisioning an average sectoral contribution of 34%, 41%, and 15% from public, private and external sources respectively from 2020 to 2030.[3]

In order to increase private sector participation in SDG financing, the government needs to carefully monitor the changing paradigm of development financing. Domestic untapped micro-savings can be one of the sources for financing development budget. Only 4% of the domestic formal savings are being invested in infrastructure at present from formal savings, whereas there are 39% of the adults who are saving through informal channels. Untapped pockets like remittances, savings, zakat and waqf funds can be tapped to finance SDG achievements.

Utilizing the Untapped Savings Market

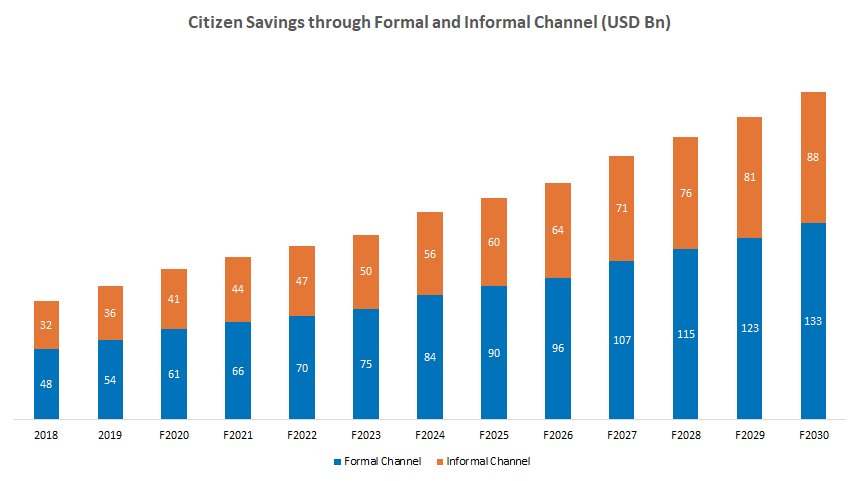

In 2019, the formal savings by Bangladeshi citizens stood at USD 54 Bn which will rise twofold within 2030 in tandem with the growth of the economy. Citizens, belonging to the informal economy, saved USD 36 Bn in 2019.[4] Growth rates for both channels are estimated to drop to 2% till 2023 in the view of COVID-19 and economic recession. Regardless, citizens are forecasted to save up to USD 88 Bn by 2030 as the economic downturn might force the middle and affluent class consumer to spend less and save more. Moreover, last year’s remittance inflow of USD 18.32 Bn was kept excluded from the formal channel. If these untapped resources can be partially aggregated and deployed through a digital financial value chain from 2020 onwards, a yearly flow of USD 45 Bn incremental can be generated to finance SDGs.

To be considered as a long term development fund, a fund needs to be scalable and stable. Fueled by the recent economic progress, an overall rise in Bangladeshi citizens’ disposable income has been observed which indicates increased scalability of citizen savings as well increase in savings (amount and frequency). Additionally, the digital ecosystem has finally come of age enabling rapid technology adoption among citizens (99% 2G internet penetration, 40 million+ on smart devices, 80 million internet users and 35 million mobile financial service accounts).

Leveraging Islamic Financing in Achieving SDGs

According to Islamic Finance News, the value of Islamic financial assets in Asia is estimated to exceed USD 1.0 trillion by 2023. Bangladesh Bank’s data reveals that Islamic banks in Bangladesh hold a 25% share of the overall banking sector.[5] This fast-growing industry is comprised of capital market instruments such as Islamic microfinance, Sukuk, Islamic insurance (Takaful) and other non-commercial instruments such as Zakat, Waqf, Sadaqah and Qard al-Hasan (interest-free loans). In 2019, the Zakat fund of USD 3.5 Bn (approx.) remained excluded from the formal financial channel. In Indonesia, the Zakat funds are being utilized efficiently and channeled towards renewable energy projects in underserved communities. In other Muslim-majority countries including Palestine, Bahrain, Turkey, initiatives related to Islamic financing are underway. It is worthwhile to mention, the national poverty rate in Bangladesh increased to 35% in 2020 from 24.3% in 2016 due to the adverse impacts of the pandemic.[6] Institutionalization of Zakat funds is an innovative process of collectively disseminating wealth that can play a pivotal role in poverty alleviation in Bangladesh as well.

Ensuring Equitable Growth through Impact Investment

To meet the ambitious SDGs in post-pandemic Bangladesh, the country needs more foreign borrowings to build up the country’s forex reserve and focusing on impact investment can be just the right way to do it. It can be a great tool to reduce the socio-economic gap and move the country closer to meeting the SDGs. The neighboring country India has displayed successful and sustainable deployment of impact capital as it received almost USD 5 billion+ impact capital from more than 50 investors over the decade.[7] Under Alternative Investments License, “Impact Funds” has been acknowledged as a separate investment type; however, to further encourage impact investing, the formation of Social Impact Bonds is of utmost importance. This would satisfy the need for the public good by which private capital mobilization would be facilitated and measurable impact will be witnessed. In addition, proper guidelines to qualify as an impact enterprise and regulations for financial institutions would further ease the process of getting into impact investments.

Sustainable Financing to Attain SDGs

Through public-private partnerships, good governance and co-ordination of investment green financing can drive the country towards a green economy. Green industrial policies are much needed to materialize the opportunity that will set standard outcomes for companies including reducing carbon emissions, increasing resource efficiency, pollution control, or adoption of ecosystem services. To enhance the system, “green bonds”, bonds that exclusively finance low carbon and climate-resilient projects, can be developed to encourage investors. International Finance Corporation (IFC) identified key areas of concern related to financial sector development for Bangladesh where green financing has been highly stressed. The creation of a national green bond market will help the country become a circular economy achieving resource efficiency and explore the country’s climate-smart investment potential of USD 172 Bn by 2030.[8]

Financial instruments and mechanisms like securitization, micro insurance, crowd-funding can be leveraged with digital technology in creating the digital financial value chain. The proposed platform will bridge the gap between micro savers and the government resulting in a low-cost source for long terms with its related disintermediation, distribution effect, transparency and accountability features. For instance, a citizen can invest in the construction of a bridge and later will be paid back from the earning proceeds.

Overarching Issues in Adapting an Alternative Financing Model and Ways to Overcome

SDGs cannot be achieved in silo and thus all relevant agencies such as regulatory bodies, digital financial service providers, telecommunication companies, non-profit organizations, private sector players and financial institutions must work together to bring about the change. Initial resistance from citizens due to lack of proper financial knowledge will be one of the primary challenges in implementing the alternative financing method. However, the collaboration between public and private sector players in educating the citizens can play a significant role in developing the ecosystem. In the implementation phase, the government and related agencies might face some obstacles as well. In order to mitigate the chance of failure in the deployment phase i.e. inability to target aggregated funds to specific SDGs, two practices can be followed – piloting before implementation and ensuring accountability of involved agencies.

Bangladesh was ranked 109th among 162 nations in the 2020 SDG index.[9] Although the country has achieved remarkable progress since 2016, it still has a long way to go. Backed by proper regulatory support from the policymakers, technology implementation support from digital financial service providers and telecom companies, a domestic capital market can be built in Bangladesh which will play an instrumental role in meeting the SDGs. Creation of a mega fund by aggregating citizen savings does not only mobilize private financing in achieving the SDGs but, most importantly, it catalyzes innovative new approaches to social and environmental challenges and creates an unparalleled distributional effect in the economy.

References

- 1. An Analysis of the National Budget for FY2020-21– Centre for Policy Dialogue

- 2. Secretary, Economic Relation Department – ERD

- 3. Bangladesh Sustainable Development Goals (SDGs) Progress Report 2020 – UNDP Bangladesh

- 4. Global Findex Report 2017 – World Bank

- 5. Islamic transactions snare 25pc of country’s total banking assets – Financial Express

- 6. Growth, poverty and inequality implications of Covid-19 – Centre for Policy Dialogue

- 7. IMPACT INVESTING: NEW FRONTIER FOR BANGLADESH? – LightCastle Partners

- 8. SBN Necessary Ambition: Country Profile Bangladesh – International Finance Corporation

- 9. Sustainable Development Report 2020 – Sustainable Development Solutions Network